The Oil Shock Is Old News. The Food Shock Is Coming.

Hormuz Isn't an Energy Story Anymore — It's a Grocery Store Story

The oil price headlines have been running for two weeks now and you’ve absorbed them. Brent crude above $85. WTI whipsawing on false reports about Navy escorts. Goldman’s $135-per-barrel scenario if the closure persists for four months. The graphs go vertical, then partially correct, then climb again. You understand the story.

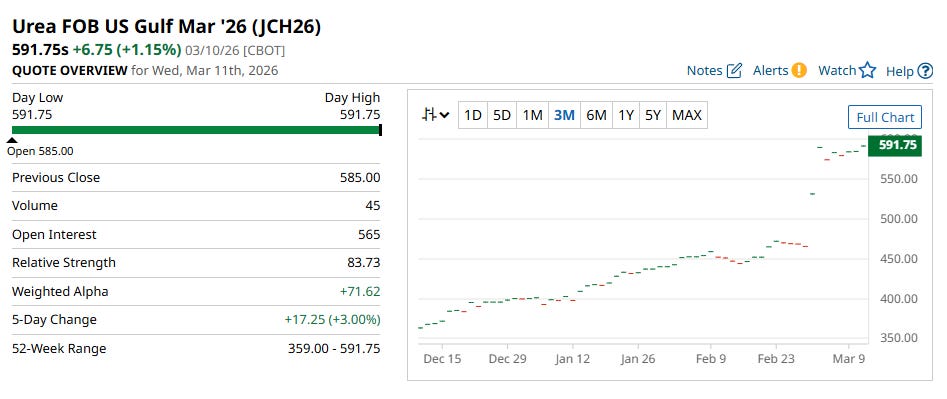

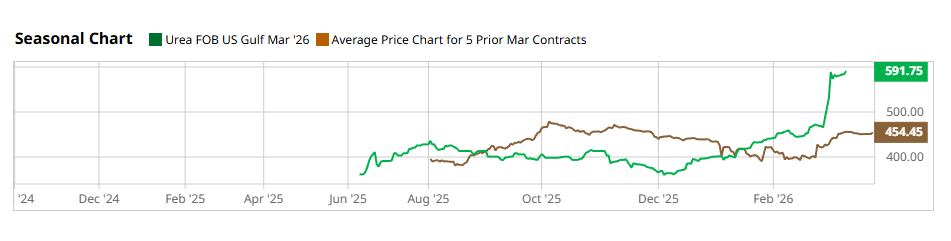

Here’s what I want you to pay attention to instead: urea prices at the New Orleans hub have moved from $475 per metric ton to $579+ per metric ton in the past ten days. For context, urea spent most of 2025 trading between roughly $350 and $450 per metric ton. A move from $475 to nearly $580 in ten days is not routine volatility — it’s a supply shock signal.

You may not know what urea is. That’s fine. It’s fertilizer — specifically, the nitrogen fertilizer that covers a substantial portion of American corn and soybean production. The Midwest planting window opens in April. And roughly one-third of the global fertilizer trade transits the Strait of Hormuz.

The oil shock is a financial event. It moves markets in real time. It triggers reserve releases, G7 emergency calls, and JPMorgan stress scenarios. It’s visible, it’s tracked, it’s argued about on every financial terminal in the world. Smart people are watching it carefully.

The food shock is a physical event. It doesn’t move in real time. It moves through supply chains, through planting decisions made in the next thirty days, through harvest yields in September, through price adjustments that show up in grocery stores next winter. It doesn’t respond to reserve releases. It doesn’t care about press secretaries or G7 coordination calls. It operates on agricultural time, which is slower than financial time and has more permanent effects.

Almost nobody is talking about it. And that gap — between the visibility of the oil story and the invisibility of everything downstream of it — is what this piece is about.

The Transmission Mechanism Nobody’s Running

Supply disruptions don’t hit consumers directly. They hit them through transmission chains — sequences of industrial dependencies that convert a disruption at one node into price and availability effects at other nodes, often weeks or months later. The chain from a closed strait to a higher gas price is short and well understood. The chains that run through fertilizer, LNG, petrochemicals, packaging materials, and food — those chains are longer, less visible, and operate on timelines that most current commentary doesn’t track.

Consider what’s actually moving through the Strait of Hormuz, or rather, what stopped moving.

Qatar, one of the world’s largest LNG producers, halted production after Iranian drone strikes hit its Ras Laffan and Mesaieed industrial facilities in the first week of the conflict. Qatar supplies approximately 12–14% of Europe’s LNG. That production halt’s effects on European industrial energy costs will compound through European manufacturing input prices over the next 30–60 days. European manufacturers whose energy costs are rising will pass those costs through to the products they sell. Some of those products come back to the United States. Some of them are inputs to American manufacturing.

Aluminum is in the chain. The Middle East is a significant supplier of aluminum and aluminum inputs to global manufacturing, and those supply chains run through Hormuz.

Petrochemicals are in the chain: approximately 85% of polyethylene exports from the Middle East transit this strait. Polyethylene is the feedstock for most plastic packaging — the wrapping on medicine, food, electronics, and household goods. When petrochemical supply tightens, the cost of packaging rises, and that cost quietly propagates into the price of almost everything on a retail shelf.

And, again, there’s the fertilizer. Urea, anhydrous ammonia, and diammonium phosphate — the primary nitrogen and phosphate fertilizers in global agriculture — are heavily produced in Persian Gulf countries and heavily transited through the strait. Prices have already moved. Nitrogen fertilizer is essentially natural gas converted into crop yield. When LNG supply shocks hit gas markets, fertilizer prices follow.

Here is the critical timing issue: the Midwest planting window for corn and soybeans opens in April and closes in late May. It is not a flexible deadline.

Farmers facing a 43% increase in input costs over a six-week window before planting must decide: absorb the cost and plant on schedule, compressing already-thin margins; reduce fertilizer application and accept yield degradation; or delay planting and accept both outcomes. There is no reserve mechanism for fertilizer. There is no SPR equivalent that releases nitrogen onto the market at pre-crisis prices. The agricultural transmission is operating on its own clock, and the clock is running.

What the Market Is Getting Wrong

Markets are currently pricing the Hormuz closure as a recoverable event. The assumption built into current commodity prices is that a diplomatic or military resolution comes quickly enough to prevent second-order supply chain disruptions from compounding. Tuesday’s oil price volatility — the 19% plunge on the Energy Secretary’s false report of a Navy escort, the partial recovery when the White House corrected him — illustrates the bet the market is making: this ends, and it ends soon.

That bet may be correct. Trump has threatened strikes twenty times harder if Iran disrupts oil flows. The G7 convened. The IEA announced a 400-million-barrel reserve release. Diplomatic back-channels are presumably running. These are real mechanisms.

But notice what those mechanisms don’t address: the fertilizer transmission to the spring planting window. The LNG production halt at Qatar’s facilities. The petrochemical supply disruption to global manufacturing. These don’t get fixed by a ceasefire announcement. The disruption has already occurred. The goods that were supposed to move through the strait in the first two weeks of March didn’t move. The industrial processes that depended on them have already adapted — and those adaptations are now embedded in prices, production schedules, and planting decisions for the next several months, regardless of what happens to the military situation.

The oil shock can be partially addressed with reserve releases. The food and materials shocks largely cannot. The transmission is already in motion, operating below the visibility threshold of financial markets, on agricultural and industrial timelines that don’t respond to the same interventions that calm oil trading.

There is a specific irony embedded in this: ExxonMobil’s chief economist said last week that it had been “consensus last week, and to a certain extent still today,” that everyone but Russia has “an interest in normal traffic resuming through the Strait of Hormuz.” He’s right about the interest. He’s wrong to say that shared interest is sufficient to stop downstream transmission. Supply chains don’t care about shared interests. They respond to physical disruptions, and one has already occurred.

The market is underweighting the duration risk. Not the probability of the strait reopening — it probably does, eventually — but the lag between reopening and restored supply chain function. Reopening the strait doesn’t restore Qatar’s LNG production on day one. It doesn’t lower urea prices back to $475. It doesn’t recover the two weeks of missing petrochemical supply. It restarts the clock on restoration, which itself takes weeks to months.

More importantly, there is a second-order implication here that markets miss.

Oil shocks hurt economies. Food shocks destabilize societies.

When oil rises, households adjust. They drive less. They complain about gas prices. Politicians release reserves and blame OPEC. The economy slows, but the system absorbs the shock.

Food operates differently. Food is not discretionary spending. It is the base layer of the household budget. When the price of bread, rice, or cooking oil rises sharply, the effect is immediate and political. Households cannot substitute away from calories.

History reflects this pattern with uncomfortable consistency. The food price spike of 2007–2008 contributed to unrest across North Africa and the Middle East. The second spike in 2010 preceded the Arab Spring. Governments survived oil shocks throughout the twentieth century; many did not survive sudden increases in staple food prices.

The reason is simple: food inflation hits the lowest-income households first and hardest. When fertilizer prices move today, the consequences don’t show up in energy trading desks or central bank briefings. They show up months later in the price of corn, soybeans, animal feed, and cooking oil. By the time those effects reach consumers, the transmission mechanism is already complete.

And unlike oil markets, there is no equivalent of a strategic fertilizer reserve that governments can deploy to reverse the process. Once planting decisions are made and yields are locked in, the system runs forward to harvest.

That is the lag embedded in the current situation. The oil shock is visible and heavily debated. The food shock — if fertilizer prices remain elevated into the planting window — is already working its way quietly through the system.

By the time it becomes visible in food prices, the decisions that caused it will be months in the past.

What you’re watching is not just an oil price event.

It’s the beginning of a multi-month inflation transmission that cannot be recalled.

What a Rational Person Does With This

The question every reader of this publication is already sitting with, stated plainly: fine, I understand the structural argument. What do I actually do?

The honest answer to the immediate transmission: most of the food inflation that’s been set in motion is not something you can personally hedge in a way that meaningfully protects you.

You can stock staples. You can focus on food sources that aren’t exposed to global fertilizer pricing — local farms, your own garden, protein sources with shorter supply chains. These are not useless steps. They’re also not sufficient to materially insulate your household from a 43% nitrogen fertilizer price increase compounding through your food supply over the next twelve months.

What you can address is the broader implication.

The systemic fragility that allowed a thirteen-day disruption to a twenty-one-mile-wide waterway to threaten European LNG supply, American corn planting, global packaging manufacturing, and household inflation expectations is not an anomaly. It is the architecture.

The concentration of global industrial supply chains through a small number of geographic chokepoints, operating on minimal inventory buffers, governed by institutions whose credibility and coordination capacity are actively degrading — that geometry persists regardless of how this specific conflict resolves.

This is the “why now” argument for people who’ve been asking themselves how bad it actually needs to get before jurisdictional optionality moves from planning concept to actionable priority.

The structural case for building a sovereign stack — residency optionality in a stable jurisdiction, assets that aren’t entirely denominated in a currency whose purchasing power is exposed to every chokepoint crisis, legal and financial standing that doesn’t depend on any single country’s institutional integrity — was not built on the prediction that any specific crisis would trigger action. It was built on the observation that the architecture generating these crises is structural and persistent, and that the latency cost of waiting to act is not zero.

What the Hormuz closure has done is make that argument visible in a way it wasn’t visible on February 27. A Cabinet secretary posted false military information and moved oil markets 19% with zero institutional cost. Food prices are going to rise because a drone hit a gas facility. The G7 convened. The IEA released reserves. And the system that produced all of it is running on the same architecture as before the first strike.

The families who have been building optionality during the period when this was an “eventually” problem have something the rest of the field doesn’t: time and deliberateness. They made decisions when the information environment was calm enough to make them well. They weren’t responding to a crisis; they were preparing before one. That preparation gap — between people who’ve been in motion and people who are starting from zero — doesn’t close quickly.

The argument for moving from analysis to planning is not panic. It’s not a bet on catastrophe. It’s the recognition that the window for deliberate, low-urgency sovereign planning is not permanently open, and that the cost of acting before you have to is lower — financially, logistically, emotionally — than the cost of acting after the urgency is undeniable.

If you’re ready to move from analysis to action, the frameworks for evaluating specific jurisdictions, building a sovereign stack appropriate for your income profile and family situation, and sequencing the practical steps without sacrificing the rest of your life in the process — that’s what Borderless Living is for. The Spain vs. Italy framework went up yesterday. The BSI country profiles are in the archive. The Concierge service is for families who want experienced guidance to hold the pieces together.

The transmission is in motion. The question is whether you use the time before it arrives at your grocery store to build something or spend it watching the oil price chart.

It is not just food or oil shocks. This war has screwed the existing global economy because almost 100% of any good that we consume or use in North America has embedded fossil fuels (or emissions). Electricity, manufacturing components and processes and transportation use fossil fuels. Here is a link to a Siemens blog which explains the problem in terms of emissions, https://blogs.sw.siemens.com/simcenter/embedded-emissions-the-carbon-cost-of-everything/

Whatever happens in the Middle East, fossil fuels will become far more expensive and they are not renewable. So, as a society we may need to re-evaluate how we use this precious resource. In the meantime, we may find ourselves living as we did in the 1960s or earlier while trying to build renewable energy and build resilience against climate change. (I have no doubt that the Project 2025, Trump and his tech bros will claim that the remaining fossil fuels should be used for military and defense purposes at the expense of the livelihood and health of the American public, and perhaps the rest of the world.)

The sooner we face that our global economy is in for an enormous shift and that those best prepared to weather it with concrete ideas on the way forward are those states from the global south. Secretary General Guterres has been calling for the restructuring of multilateral institutions so that they can address global inequality and climate change on a fast track. It is time to really listen and do just that.

I'm betting the couchfucker (<-one word or two?) has a hard-on thinking about all that farmland he and his bros are gonna hoover up, pennies on the dollar...